Wolfspeed Inc. (WOLF) – High-Risk, High-Reward Turnaround Bet

Investment Thesis Overview

Wolfspeed Inc. (WOLF) represents a highly speculative but potentially asymmetric opportunity. While the company is undergoing a Chapter 11 restructuring, the underlying business remains strategically positioned in the growing silicon carbide (SiC) semiconductor space. If Wolfspeed successfully exits bankruptcy and restructures its debt, it could experience a dramatic revaluation — particularly due to its extreme short interest and recent signs of institutional accumulation.

This is a speculative turnaround and short-squeeze candidate with meaningful upside if the business survives.

The Core Bet

This is not a value investment — it is a calculated, high-risk position built around a potential corporate recovery, deleveraging, and short squeeze. The Chapter 11 filing was not for liquidation, but for balance sheet restructuring. If successful, equity could retain value or be diluted less severely than feared. Given the record levels of short interest, any positive surprise could result in a sharp price spike.Why It’s Interesting now.

a. Pre-Packaged Chapter 11 Filing

- Wolfspeed entered Chapter 11 with a restructuring plan already approved by over 97% of secured creditors and more than 67% of bondholders.

- This greatly increases the odds of a fast and orderly exit from bankruptcy.

- Interest expenses are expected to drop by over 60%, offering the company breathing room and a path to return to profitability.

b. Massive Short Interest

- As of July 2025, short interest exceeds 49% of the float.

- Borrow fees are well above 400% annualized — indicating significant cost pressure on short sellers.

- In such setups, any unanticipated bullish catalyst (e.g., early exit, new investor, government aid) could force rapid covering and create a squeeze.

c. Undervalued Optionality in a Strategic Industry

- Wolfspeed remains a major player in the silicon carbide (SiC) semiconductor space, which is critical to electric vehicles (EVs), renewable energy systems, and high-efficiency power electronics.

- Global SiC demand is expected to grow more than 5x by 2030 as energy efficiency and electrification trends accelerate.

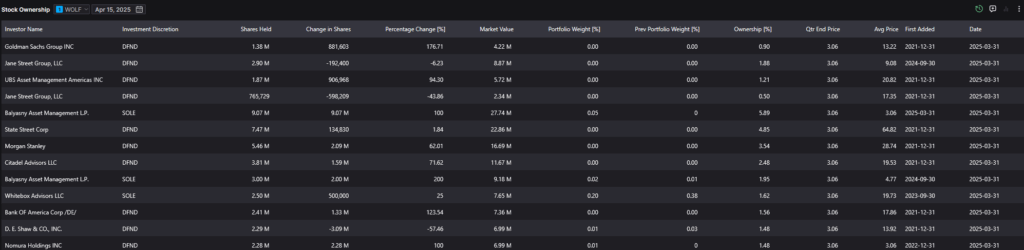

d. Institutional Accumulation at Higher Prices

- In March 2025, both Goldman Sachs and Jane Street disclosed significant share purchases.

- Their average buy-in was reported at approximately $13.22, compared to the current price of around $1.43.

- While they may be positioning for arbitrage, debt-equity swaps, or restructuring involvement, it adds credibility to the upside case.

Risks

Investors should fully understand that this is a speculative bet with high downside potential. Key risks include:

- Common equity could be wiped out entirely in the restructuring.

- Delays or breakdowns in the Chapter 11 exit plan.

- Continued operational losses post-bankruptcy.

- Poor macro conditions affecting semiconductor demand.

- Regulatory or legal complications during the restructuring.

This investment should only be made with money you can afford to lose, and with a clear exit plan in place.

Upside Scenarios

Base Case: The company exits Chapter 11 in late 2025, resumes operations, and recovers to the $3–5 range.

Bull Case: Successful exit combined with positive guidance and new contracts pushes shares toward the $8–12 range.

Squeeze Case: A short squeeze triggered by news, meme-stock interest, or positive restructuring results drives a fast 5–10x move in a matter of days or weeks.

Why KCapital Is Taking a Position

At KCapital, we specialize in asymmetric bets where the potential reward vastly outweighs the capital at risk. Our position in WOLF is intentionally small, tightly risk-managed, and based on a clear setup:

- An oversold equity with extreme short interest.

- Institutional activity at much higher price levels.

- A bankruptcy plan that is pre-approved and progressing toward resolution.

- A business that remains aligned with long-term megatrends in electrification and energy efficiency.

This position is not based on fundamentals or intrinsic value — it’s a thesis on optionality, crowd behavior, and turnaround execution.

Final Thoughts

Wolfspeed is a high-volatility, high-uncertainty play — but it sits at the intersection of real industrial value and distressed-market inefficiency. If the company survives and equity holders retain value, the upside could be significant. While the risks are very real, the reward is potentially transformational for a small, calculated bet.

As with any distressed equity, sizing, timing, and emotional discipline are key. This is not a buy-and-hold play — it’s a special situation trade with risk-managed intent.